Introduction

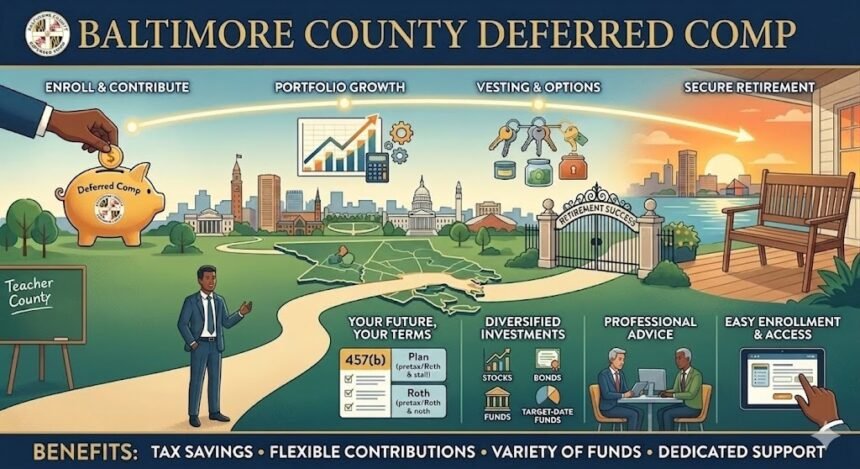

Planning for retirement can feel overwhelming, right? You’re juggling work, family, bills, and somehow need to think about decades from now. That’s where the Baltimore County Deferred Comp steps in. It isn’t just a savings program it’s a tool to help you take control of your financial future.

The beauty of deferred compensation plans is that they let you grow your money while delaying taxes, giving your savings more room to breathe and multiply over time. But navigating the ins and outs can seem confusing at first. Don’t worry, we’ll break it down, step by step, and show you how to make the most of it while keeping things practical and realistic.

What Exactly is Baltimore County Deferred Comp?

At its core, the Baltimore County Deferred Comp is a retirement savings plan designed for county employees. It allows participants to defer a portion of their salary into a tax-advantaged account. The money grows over time, potentially giving you a comfortable cushion for retirement.

Unlike standard pension plans, deferred comp plans give you more flexibility and control. You choose how much to contribute, how to invest it, and when to withdraw. It’s all about empowering your future self to have financial freedom.

Why Employees Should Consider Deferred Comp Options

Let’s face it—retirement planning is often pushed to the back burner. But participating in a deferred comp plan early can make a huge difference. Even modest contributions can grow exponentially over time thanks to compounding.

Moreover, the tax benefits are hard to ignore. By deferring income, you reduce your taxable salary today, which can also help with budgeting. And when the money grows, you won’t be taxed on those gains until you withdraw them, ideally when your tax rate is lower in retirement.

Contribution Strategies for Baltimore County Deferred Comp

The flexibility of the Baltimore County Deferred Comp plan is one of its biggest draws. You get to decide how much to contribute from each paycheck, allowing you to tailor it to your financial situation.

Contributions can be pre-tax or Roth, depending on your tax planning strategy. Pre-tax contributions reduce your current taxable income, while Roth contributions let your withdrawals in retirement be tax-free. The choice depends on whether you expect your tax rate to be higher or lower in the future.

- Start small if necessary; even 1-2% of your salary makes a difference

- Increase contributions gradually, ideally during raises or bonuses

- Consider maxing out contributions if financially possible for faster growth

Investment Options Within the Plan

Choosing where to invest your deferred comp funds is crucial. Baltimore County Deferred Comp offers multiple options ranging from conservative to aggressive. This flexibility allows participants to align investments with their risk tolerance and retirement timeline.

Understanding your options is key. Riskier investments might offer higher growth, but they come with potential ups and downs. Conservative choices protect your principal but may grow slower. Balancing risk and reward is essential for long-term success.

- Target-date funds designed for specific retirement years

- Balanced funds that mix stocks and bonds

- Equity funds for growth-focused participants

- Fixed income or stable value funds for lower-risk profiles

The Tax Benefits of Baltimore County Deferred Comp

Deferred comp plans aren’t just about saving money—they’re about saving smartly. Contributions are often pre-tax, reducing your current taxable income. This can ease your monthly budget while letting your investments grow tax-deferred.

When you eventually withdraw funds in retirement, you pay taxes at that time. Ideally, you’ll be in a lower tax bracket than during your working years, maximizing the tax advantage. Roth contributions, if available, work differently: you pay taxes upfront, but qualified withdrawals are tax-free.

How to Maximise Your Baltimore County Deferred Comp

Getting the most out of your deferred comp requires strategy. Simply contributing a fixed amount isn’t always enough to optimise your retirement. Consider increasing contributions as your salary grows, reviewing your investment allocations regularly, and taking advantage of employer match programs if available.

Regular check-ins are crucial. Life changes, market shifts, and personal goals can all affect how much you should contribute and how your investments are allocated. Staying proactive ensures you don’t miss opportunities to grow your nest egg efficiently.

Common Mistakes to Avoid in Deferred Compensation

Even experienced investors can slip up when managing deferred comp accounts. Common mistakes include contributing too little, ignoring investment diversification, or failing to monitor account performance.

Another trap is withdrawing funds too early. Not only can you face penalties, but you may also lose the compounding growth potential. Avoiding these pitfalls requires discipline and a clear plan.

- Underestimating the power of compounding over decades

- Failing to rebalance investments based on risk tolerance

- Not adjusting contributions during salary changes

- Early withdrawals without understanding penalties

Steps to Enrol in Baltimore County Deferred Comp

Starting your deferred comp plan doesn’t have to be intimidating. Baltimore County makes the process relatively straightforward, with clear guidelines for eligible employees.

- Verify eligibility as a county employee

- Choose contribution type (pre-tax or Roth)

- Decide contribution amount per paycheck

- Select your investment allocation

- Complete enrolment forms and submit

Starting early, even with a small contribution, can have significant long-term benefits. Don’t wait every dollar counts when compounding over decades.

Monitoring and Adjusting Your Plan

Once enrolled, don’t just set it and forget it. Regularly reviewing your Baltimore County Deferred Comp account ensures your contributions and investments align with your goals.

Market fluctuations, life changes, and retirement goals evolve over time. Periodically rebalancing your portfolio and adjusting contributions ensures you remain on track. A proactive approach can make a world of difference when you reach retirement.

- Schedule annual or semi-annual portfolio reviews

- Adjust contributions after salary changes or bonuses

- Rebalance your investments to maintain your desired risk level

- Stay informed about plan updates or new investment options

Conclusion

Baltimore County Deferred Comp is more than just a retirement plan it’s a strategic tool for securing your financial future. By taking control of contributions, selecting investments that match your goals, and monitoring progress regularly, you can build a retirement plan tailored to your needs. Start early, stay consistent, and leverage the tax advantages to your benefit. With thoughtful planning and active management, Baltimore County Deferred Comp can help you reach a comfortable and confident retirement while giving you peace of mind along the way.

FAQs About Baltimore County Deferred Comp

1. Who is eligible for Baltimore County Deferred Comp?

Eligible employees include full-time and part-time county employees meeting specific employment criteria.

2. Can I choose between pre-tax and Roth contributions?

Yes, participants can select either pre-tax contributions to reduce current taxable income or Roth contributions for tax-free withdrawals in retirement.

3. How do I select investments for my deferred comp?

Options typically include target-date funds, equity funds, balanced funds, and fixed-income funds. Choose based on risk tolerance and retirement goals.

4. Can I change my contribution amount or investment allocation?

Yes, adjustments can be made periodically to accommodate salary changes, bonuses, or shifts in retirement objectives.

5. Are there penalties for early withdrawals?

Yes, early withdrawals may result in taxes and penalties, reducing the benefits of long-term compounding.